Smart Retirement Planning Tips Every Woman Should Know 💛

Some links in this post are affiliate links. As an Amazon Associate, we earn from qualifying purchases that help keep our content free.

Retirement doesn’t have to feel confusing or overwhelming. With the right plan, it becomes a season of freedom, confidence, and everyday joy. In this guide, I’ll walk you through the Smart Retirement Planning Tips every woman should know, using simple language, practical steps, and clear explanations that actually make sense.

Whether you’re dreaming of early retirement, wondering when to retire, or trying to understand Social Security Benefits, this post will help you build a retirement plan that feels grounded, exciting, and completely doable — no stress, no jargon, just clarity and confidence for your future. Let’s create the retirement you truly deserve. 💛

Retirement Planning Tips

The strongest retirement plan is simple, realistic, and grounded in clarity. These Retirement Planning Tips will help you understand exactly where you stand, what you need, and how to build a future that feels financially secure and joy-filled. We’ll walk through lifestyle planning, formulas that make the math easy, health insurance considerations, and smart Retirement Strategies that set you up for long-term peace of mind.

1. Start With Your Lifestyle Equation

Your retirement plan begins with one big question:

What life do you want to live?

Your lifestyle determines your budget — not the other way around. To get clear, imagine:

• Where you want to live

• How much you travel

• Daily and weekly retirement activities

• Home costs

• Food and wellness routines

Write this vision in a guided retirement journal to create your baseline.

2. Calculate Your “Retirement Number” With Two Simple Formulas

You don’t need a degree in finance. Use these two formulas to understand how much money you need.

Formula A: The 25× Rule (simple baseline)

Annual spending × 25 = Target nest egg

Example:

$50,000 annual spending × 25 = $1.25M needed

This is based on the long-term “safe withdrawal rate” and is a helpful starting point.

Formula B: The Monthly Gap Formula (more personalized)

Monthly expenses – Guaranteed income = Monthly gap

Monthly gap × 12 × 25 = Estimated nest egg needed

Where guaranteed income includes Social Security, pensions, annuities, rental income.

Using a Retirement Calculator helps double check your number, giving you confidence and clarity.

3. Estimate All Retirement Costs (Including the Ones Most People Forget)

Most women underestimate retirement costs. Here’s a clear list to guide you:

Core living costs

• Housing or mortgage

• Insurance (home, car, life)

• Utilities

• Food

• Transportation

Medical & health insurance (essential!)

This is often the biggest surprise. Include:

• Medicare premiums

• Medigap or Medicare Advantage

• Prescription drugs

• Dental and vision (not fully covered by Medicare)

• Unexpected medical events

• Long-term care (assisted living, home health support)

Tip: Set aside a yearly medical cushion in your Retirement Budget. Most planners estimate $6,000–$12,000 per person per year depending on health.

Often-forgotten retirement costs

• Home repairs

• New glasses/hearing aids

• Travel to see family

• Pet care

• Technology (laptop, phone replacements)

• Hobbies and memberships

• Gifts and celebrations

These are joyful costs — plan for them so you can say yes without stress.

4. Build a Practical Money Saving Plan

Your Money Saving Plan doesn’t need extreme budgeting. It just needs consistency.

Here’s a method that works beautifully:

The “10-20-70 Method” (easy & joyful)

• 10% → savings

• 20% → investing/retirement

• 70% → daily life

If your income doesn’t allow 10–20–70 right now, adjust the percentages. Consistency matters more than perfection.

Automations help:

• Auto-transfer to savings

• Auto-contribute to your 401K

• Auto-invest into low-cost index funds or target-date funds

Using digital budgeting planners or printable money trackers keeps this effortless.

5. Strengthen Your Retirement Strategies (Your Long-Term Power)

Smart Retirement Strategies include:

A. Maximize your 401K or IRA contributions

If your employer matches your 401K, always contribute enough to get 100% of the match. It’s free money.

B. Reduce high-interest debt before retiring

Debt is a silent budget killer. Paying it down opens up cash flow for joy.

C. Invest simply through low-cost index funds

Index funds grow your money long-term with very little maintenance.

This aligns perfectly with beginners and long-term peace of mind.

D. Build a 6–12 month emergency fund

This covers unexpected medical or life expenses without stress.

E. Track your progress yearly

Review:

• Cost of living

• Health insurance

• Savings rate

• Investments

• Income streams

Use a notebook or a simple digital retirement planner to stay organized.

6. Create a Retirement Budget You Can Actually Live With

Your Retirement Budget should feel supportive, not restrictive.

Create 3 categories:

Needs: housing, food, insurance, medical care

Wants: travel, dining out, hobbies

Dreams: big vacations, home upgrades, creative projects

This structure makes Retirement Planning Insights simple and keeps your money aligned with what brings joy.

7. Test-Run Your Plan Before You Retire

One of the smartest retirement advice strategies is this:

Live on your projected retirement budget for 3–6 months while you’re still working.

It shows you:

• If the budget feels realistic

• Where you overspend

• What needs adjusting

• How prepared you truly are

This test-run removes fear and replaces it with calm confidence.

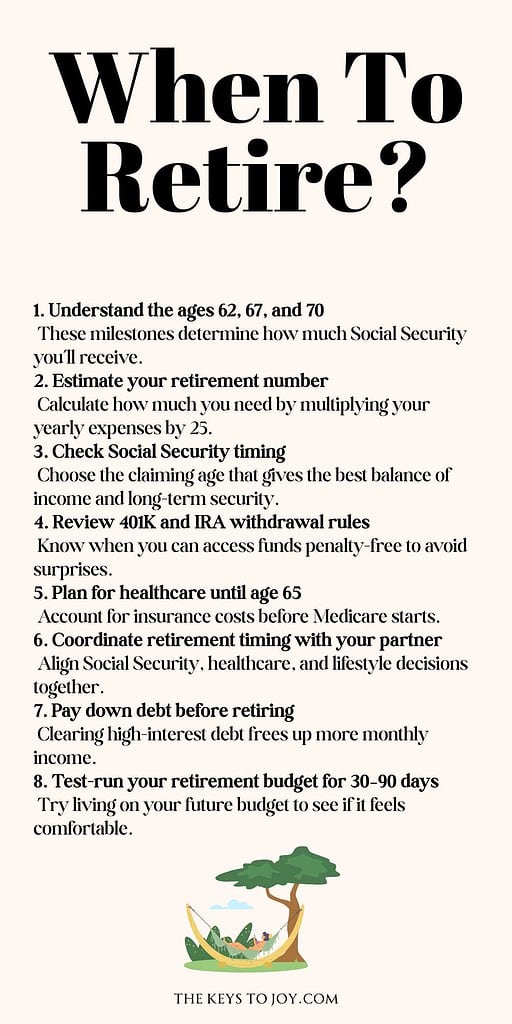

When to Retire

Choosing when to retire isn’t just a date on a calendar — it’s a blend of financial readiness, lifestyle goals, health, and the resources available to you and your partner. This chapter walks you through the essential factors so you can make a confident and informed decision. We’ll break down income streams like Social Security Benefits Retirement, your 401K, partner benefits, healthcare timing, and key milestones that help you pinpoint the right moment.

1. Understand Your “Retirement Readiness Number”

Before deciding when to retire, you need to know:

Do I have enough to maintain my lifestyle for the next 25–30 years?

Use this simple formula:

Annual retirement spending × 25 = Target nest egg

or for couples:

(Combined annual spending – guaranteed income) × 25 = Joint target nest egg

Guaranteed income includes:

• Social Security Benefits Retirement

• Pensions

• Rental income

• Annuities

This is your baseline. It tells you whether you’re close, comfortably ready, or need more time.

2. Know Your Social Security Milestones

The age you claim Social Security Benefits Retirement has a huge impact on lifetime income.

Here are the key ages:

62 — Earliest claim, but permanently reduced benefits

67 — Full Retirement Age (FRA) for most people today

70 — Maximum benefit (about 8% increase for each year you delay past FRA)

General rule:

If you have strong health, longevity in your family, or other income sources (like a 401K or IRA), delaying until 70 often gives the best long-term value.

For couples:

• The higher earner delaying to 70 maximizes survivor benefits

• Coordinating timing creates thousands of dollars in lifetime value

• Lower-earning spouses can claim spousal benefits at FRA

Understanding these milestones helps you choose the most financially powerful retirement date.

3. Check Your 401K Timeline and Withdrawal Strategy

Your 401K and other retirement accounts play a big role in When To Retire.

Here are the big rules to know:

59½ — You can withdraw from IRAs and 401Ks without penalty

55 — If you retire at this age (or after) from your current employer, you may withdraw from that employer’s 401K without the penalty

73 — Required Minimum Distributions (RMDs) begin

This affects your budget and withdrawal plan.

Many women retire when their 401K has reached a steady growth curve and Social Security is close enough to bridge the gap. A yearly review of your account balance and growth (a key part of Retirement Planning Insights) will tell you when you’re financially strong enough to step into retirement.

4. Estimate Health Insurance Costs Before Medicare Kicks In

Healthcare is often the biggest “hidden cost,” and it heavily influences your retirement date.

Here’s what you need to plan for:

Before 65 (not yet eligible for Medicare)

• Marketplace health insurance (often expensive)

• Employer-sponsored retiree coverage (rare but valuable)

• COBRA (temporary and expensive)

• Out-of-pocket costs, dental, vision, prescriptions

At 65

• Medicare begins

• Choose between:

– Original Medicare + Medigap

– Medicare Advantage

• Prescription coverage (Part D)

• Dental + vision plans still needed

Many people wait until 65 to retire because healthcare becomes affordable.

If you want Early Retirement, your Money Saving Plan must include a clear healthcare budget.

5. Consider Your Partner’s Retirement Timing

Your partner’s plan affects your own Retirement Strategies in powerful ways:

Income coordination

• One partner working may cover healthcare and add income, allowing the other to retire earlier

• Two incomes ending at the same time can create a sudden budget shift

Social Security coordination

• The higher earner often delays claiming

• The lower earner may benefit from spousal benefits

• Survivor benefits become stronger when the higher earner delays

Lifestyle coordination

• Do you want to retire at the same time?

• Would you enjoy a “phased retirement” where one retires earlier?

• What daily rhythm works best for your relationship?

Retirement is a team plan — even if one person steps out of the workforce first.

6. Factor In Debt, Savings, and Your Timeline Cushion

Your financial strength includes:

• Remaining mortgage balance

• Car loans

• Credit card debt

• Monthly spending

• Emergency fund

• Investment growth potential

Ready to retire? Here’s a simple test:

If your savings could cover at least 25–30 years of spending — including medical costs — without running out, you’re in a strong position.

Many planners recommend having:

• Mortgage fully paid off or a clear plan for the remaining years

• No high-interest debt

• A 6–12 month emergency fund

• A steady withdrawal plan (4% rule or bucket strategy)

7. Use a “Trial Retirement Month” to Test Your Date

Before you commit to your retirement date:

Live one full month on your projected retirement budget.

Pretend your income is:

• Social Security

• Withdrawals from your 401K or IRA

• Partner’s income (if any)

• Other savings

This “trial run” reveals:

• Whether the budget feels comfortable

• How much flexibility you need

• Whether your retirement date feels right or needs adjusting

It’s one of the smartest pieces of retirement advice.

How To Know If You’re Ready To Retire

Deciding if you’re truly ready to retire is one of the biggest choices of your life — and it deserves clarity, confidence, and honesty. This chapter gives you a simple, holistic way to assess your financial strength, emotional readiness, lifestyle goals, and long-term security. You’ll know exactly what to look for and which signs show you’re prepared for a joyful new chapter.

1. Your Financial Foundation Feels Stable

The clearest sign you’re ready to retire is knowing your money can support your lifestyle for the next 25–30 years. Use two simple checks:

The 25× Rule:

Your annual spending × 25 = your ideal savings target.

Your Monthly Gap Formula:

Monthly expenses – guaranteed income = your required withdrawals.

If your guaranteed income (like Social Security Benefits Retirement, pensions, or rental income) covers most of your needs — and your savings comfortably fill the rest — you’re in a strong position.

2. You Understand Your Income Streams

You know where your money will come from each month and how it fits together:

• Social Security

• 401K or IRA withdrawals

• Roth IRA tax-free funds

• Brokerage investments

• Part-time or passion income

• Savings and emergency funds

If your cash flow feels predictable and easy to manage, that’s a major green light.

3. Your Healthcare Plan Is Fully Covered

Many people don’t retire because of healthcare uncertainty. You’re truly ready when:

• You know how you’ll cover medical insurance until Medicare

• You understand Medicare costs after age 65

• You’ve budgeted for dental, vision, and prescription expenses

• You have a cushion for unexpected health issues

If your healthcare plan feels solid and affordable, your readiness level increases dramatically.

4. You’ve Paid Down High-Interest Debt

Debt doesn’t automatically prevent retirement — but high-interest debt can make it stressful.

You’re ready when:

• Credit cards are paid off

• Personal loans are low or eliminated

• Your mortgage is manageable or nearly paid down

• Monthly obligations feel light

Lower debt means higher freedom.

5. You Know Your Retirement Budget — and It Feels Good

Your Retirement Budget should support:

• Necessities

• Comfort

• Travel

• Creative hobbies

• Joyful retirement activities

• Occasional surprises

You’re ready when the numbers don’t feel tight or fragile — but steady, realistic, and enjoyable.

Bonus sign: You’ve already tried a 30–90 day test run and it felt comfortable.

6. You Have a Withdrawal Strategy You Trust

Whether you use the 4% rule, 3.5% rule, or bucket strategy, you’re ready if:

• You can explain how much you’ll withdraw yearly

• You know which accounts to use first

• You understand how to minimize taxes

• Your investment mix supports both income and long-term growth

Confidence in your withdrawal plan means confidence in your retirement.

7. You’ve Talked Through Goals With Your Partner

If you’re in a partnership, readiness also includes:

• Agreeing on when to retire

• Coordinating Social Security timing

• Planning shared healthcare and lifestyle costs

• Designing daily routines that make you both happy

If your visions match (or complement each other), you’re emotionally and logistically ready.

8. You’re Excited About How You’ll Spend Your Time

Money matters — but so does joy.

You’re ready to retire when you can answer:

“What do I want my days to look like?”

You feel excited about:

• Traveling

• Volunteering

• Hobbies

• Family time

• Learning new things

• Movement and wellness

• Creative projects

• Slow mornings and flexible days

This emotional readiness is just as important as your financial stability.

9. You’ve Prepared for Life Transitions and Longevity

You’re ready when you’ve thought about:

• How long your savings need to last

• Long-term care possibilities

• Your home setup as you age

• Emergency preparedness

• Inflation and rising costs

This doesn’t need to feel heavy — just acknowledged and planned for.

10. You Feel Calm When You Look at the Numbers

The final sign is simple:

Your retirement numbers make you feel peaceful, not anxious.

If your finances, healthcare, lifestyle vision, and long-term plan feel aligned, your body will tell you before your brain does.

Peace = readiness.

Early Retirement Tips

For many women, the dream of Early Retirement isn’t about leaving work — it’s about gaining more time, freedom, and space for the joyful life you want to create. Retiring early is possible, but it requires clarity, planning, and smart strategies that protect your future. This chapter breaks early retirement down into simple steps using real numbers, healthcare planning, withdrawal strategies, and lifestyle choices that make early financial independence feel achievable.

1. Know Your Early Retirement Number (The 25× + Healthcare Formula)

The basic rule:

Annual expenses × 25 = what you need to retire early.

But early retirement requires one extra layer:

Add projected healthcare + medical costs until age 65.

Use this formula for a more accurate early-retirement target:

(Annual spending + annual healthcare costs) × 25 = Early Retirement Number

Example:

$55,000 yearly living costs

$12,000 yearly healthcare costs

= $67,000 spending total

× 25

= $1.675M required

Tip: Run these numbers in a Retirement Calculator to get clarity and confidence.

2. Plan Your Healthcare Bridge Until Medicare (This Is Non-Negotable)

Healthcare is the biggest roadblock to Early Retirement — but once you plan for it, the path becomes clear.

Before age 65, your options are:

• ACA Marketplace insurance

Premiums vary by income. Early retirees often lower taxable income to reduce costs.

• COBRA

12–18 months of employer coverage. Usually expensive but a good temporary bridge.

• Part-time employer plans

Some retirees work 10–20 hours/week to access affordable health insurance.

• Health Savings Account (HSA) if eligible

These are powerful because:

– Contributions are tax-deductible

– Growth is tax-free

– Withdrawals for medical expenses are tax-free

If you plan to retire early, build a healthcare buffer fund to cover premiums, deductibles, prescriptions, dental, and unexpected care.

A good estimate is:

$6,000–$15,000 per year per person, depending on coverage and health needs.

3. Build a Bridge Between Retirement and 59½

You can’t access most retirement accounts penalty-free until age 59½ — unless you use special Retirement Strategies.

Here are the smartest bridge options:

A. The Rule of 55 (the secret almost nobody knows)

If you leave your job at 55 or older, you can withdraw from your 401K from that employer with no penalty.

This does NOT apply to IRAs, only to your most recent 401K.

B. Roth IRA contributions are always accessible

You can withdraw your contributions (not earnings) anytime, penalty-free.

Perfect for early retirement cash flow.

C. A taxable brokerage account

Flexible, penalty-free, and ideal for:

• dividends

• long-term tax-efficient investing

• bridging early retirement years

D. Roth IRA Conversion Ladder (advanced but effective)

Convert traditional IRA funds to Roth IRA in small annual steps.

After 5 years, each conversion becomes penalty-free withdrawals.

This is one of the most powerful early retirement tools.

4. Build a Sustainable Withdrawal Strategy

Early retirees must protect their savings from running out too early. Here are the safest strategies:

The 4% Rule (classic and simple)

Withdraw 4% of your portfolio in year one and adjust for inflation.

Works well for long-term retirees but may need adjusting for early retirees.

The 3.5% Rule (more conservative)

Ideal if you’re retiring before 55 or expect higher medical costs.

Bucket Strategy

Divide your money into:

• Cash (1–2 years of expenses)

• Bonds (5–7 years)

• Stocks (long-term growth)

This protects you from market swings and keeps withdrawals stable.

5. Reduce Your Cost of Living (The Early Retirement Accelerator)

Your cost of living determines everything.

Small lifestyle shifts create huge savings:

• Downsizing your home

• Moving to a lower-cost location

• House hacking (renting a room, partial Airbnb)

• Using travel slow-living strategies

• Reducing subscriptions

• Paying off debt early

Every dollar you save now reduces your early retirement number.

Use a Money Saving Plan with automatic transfers to keep this simple.

6. Strengthen Your Investments With Simple Growth Strategies

You don’t need complicated investments.

The best early retirement portfolios often include:

• Low-cost broad index funds (S&P 500 or total market)

• A mix of stocks and bonds based on your risk level

• Consistent contributions to your 401K, IRA, or brokerage account

• Occasional rebalancing

• A calm mindset during market dips

Focus on long-term growth, not timing the market.

This is the heart of powerful Investment Tips.

7. Plan Early Retirement as a Team (Partner, Spousal Benefits, Shared Vision)

If you’re married or in a long-term partnership, your early retirement plan becomes much stronger when you coordinate:

• Social Security benefits

Higher-earner delaying claiming boosts future survivor benefits.

• 401K & IRA contributions

Two accounts growing = powerful compounding.

• Healthcare

One partner continuing part-time work may secure affordable insurance.

• Lifestyle planning

Will you both retire early?

Will one ease out sooner than the other?

Do you share the same early retirement goals?

Talk openly, plan honestly, and create a shared vision.

8. Test Your Early Retirement Plan (The 3-Month Simulation)

Before you commit, do a 90-day test run:

- Live entirely off your projected early retirement budget

- Cover healthcare premiums out of pocket

- Stick to your planned withdrawal strategy

- Track what feels comfortable and what doesn’t

This simulation instantly reveals whether your plan works or needs adjustments — one of the smartest pieces of retirement advice.

Social Security Benefits Retirement

Understanding Social Security Benefits Retirement is one of the most important parts of building a confident retirement plan. These benefits often form a reliable foundation of your income, and knowing how they work helps you decide when to retire, how to coordinate with your partner, and how your Retirement Strategies fit together. The clearer this becomes, the easier it feels to plan your future with confidence.

1. Know Your Big Three Ages: 62, Full Retirement Age, and 70

Your age at the time you claim Social Security directly impacts how much you receive for the rest of your life.

Here are the three essential milestones:

62 — Early Claiming

• You can start receiving benefits

• Payments are permanently reduced

• Ideal only if you truly need the income early or have lower life expectancy

Full Retirement Age (FRA, usually 66–67)

• You receive your full benefit

• No reductions

• Allows access to spousal benefits at their full amount

70 — Maximum Benefit

• You receive the highest possible monthly payment

• Benefits grow about 8% per year between FRA and 70

• Highly valuable for women who expect to live longer (statistically true), and for boosting survivor benefits later

Understanding these ages helps you choose the moment that supports your future lifestyle and your Retirement Planning Tips.

2. How Your Benefit Is Calculated (Simple Version)

Social Security is based on two things:

- Your 35 highest-earning working years

- When you claim your benefit

If you work fewer than 35 years, zeros are added — which lowers your benefit.

Working a few extra years can replace those zeros and increase your payout.

This is why some women choose to work part-time instead of fully retiring early — it keeps your earning years active and boosts benefits without intense workloads.

3. Spousal Benefits (A Huge Advantage Many Women Miss)

If you’re married currently or were married for at least 10 years in the past, you may be eligible for spousal benefits.

Here’s what that means:

• You can receive up to 50% of your spouse’s benefit

• Your own benefit is always paid first, and spousal benefits fill in the gap if it’s lower

• You must wait until your FRA to receive the full spousal amount

For many couples, coordinating spousal benefits is a key part of smart Retirement Strategies — especially when one partner has higher lifetime earnings.

4. Survivor Benefits (Essential for Long-Term Security)

If your spouse passes away, you may receive the full survivor benefit, which is usually their full payment.

This makes one strategy extremely valuable:

The higher earner delaying benefits until 70 can significantly increase the survivor benefit for the younger or lower-earning spouse.

For many couples, this single decision creates tens of thousands of dollars in lifetime value and long-term peace of mind.

5. Early Retirement and Social Security

If you’re planning Early Retirement, Social Security becomes part of your long-term timeline:

• Retiring early does not mean claiming early

• You can stop working at 55, 58, or 60 and still wait until 67 or 70 to claim

• Your benefit is based on your past earnings, not whether you’re currently working

However, retiring too early may lower your benefit if you replace high-earning years with zeros.

If you’re close to 35 full working years, try to complete them — even through part-time work — to protect your long-term Social Security income.

6. Taxes on Social Security (Easy Breakdown)

Your Social Security benefits can be taxable depending on your income.

Here’s the simple formula the IRS uses:

½ of your Social Security + your other income = your combined income

If your combined income is above certain thresholds, up to 85% of your benefit may be taxable.

Your Money Management Advice and withdrawal strategy can help you stay in lower tax brackets.

For example:

• Withdrawing from Roth IRAs doesn’t count as taxable income

• Reducing brokerage withdrawals can keep your combined income lower

Smart planning creates tax savings over decades.

7. Working While Receiving Benefits (Important to Know)

If you claim before your FRA and still work:

• Your benefits may be temporarily reduced

• Once you reach FRA, your benefit will be recalculated and restored

If you wait until FRA or later to claim, you can work and earn freely without any reductions.

This is helpful for those who enjoy part-time work, consulting, or creative retirement activities.

8. How Social Security Fits Into Your Bigger Retirement Plan

Think of Social Security as the steady foundation beneath your:

• 401K withdrawals

• IRA savings

• Roth accounts

• Brokerage investments

• Partner benefits

• Healthcare planning

• Cash flow projections

• Retirement Budget

It is predictable, inflation-adjusted, and reliable — making it one of the most valuable pieces of Retirement Planning Insights.

For most women, the best approach is a balanced one:

Use Social Security as your stable income, and stretch your savings with a withdrawal plan that protects your long-term security.

Money Management Advice for Retirement

Managing money in retirement becomes much easier when you simplify your accounts, organize your income streams, and understand how to make your savings last for decades. This chapter breaks down the most important Money Management Advice into clear, doable steps so you can feel confident about your future — and still enjoy the joyful lifestyle you’re creating.

These tips blend smart budgeting, sustainable withdrawal strategies, simple investing, tax awareness, and practical systems that protect your long-term financial wellbeing.

1. Organize Your Retirement Income Streams

Most retirees use a combination of:

• Social Security Benefits Retirement

• Withdrawals from your 401K, IRA, or Roth IRA

• Pensions

• Brokerage accounts

• Part-time income

• Annuities

• Rental income

Together, they create your monthly “retirement paycheck.”

A smart plan includes:

- Listing every income stream

- Identifying which are guaranteed (Social Security, pensions)

- Listing your flexible sources (401K, brokerage, Roth)

- Matching income sources to expenses in your Retirement Budget

This gives you clarity and makes cash flow feel more predictable and peaceful.

2. Choose a Withdrawal Strategy That Protects Your Future

Your withdrawal strategy determines how long your money lasts.

Here are the clearest, beginner-friendly Retirement Strategies:

A. The 4% Rule

Withdraw 4% of your retirement savings in year one, then adjust for inflation annually.

Example:

$1,000,000 portfolio → $40,000 yearly withdrawals

B. The 3.5% Rule

More conservative. Ideal if:

• You retired early

• You expect higher medical costs

• You want a safety cushion

C. The Bucket Strategy

Divide your savings into three “buckets”:

• Bucket 1: Cash for 1–2 years of spending

• Bucket 2: Bond funds for years 3–7

• Bucket 3: Stock index funds for long-term growth

This smooths out market ups and downs and gives you peace of mind.

3. Simplify Your Investments (Complexity Creates Stress)

The best long-term portfolios are often the simplest.

A practical, low-stress approach includes:

• Low-cost index funds (S&P 500 or Total Market)

• A balanced stock/bond mix based on your comfort

• Occasional rebalancing (once a year)

• Avoiding emotional decisions during market dips

Simplicity supports your confidence, especially during uncertain markets.

This approach matches beautifully with the bold Investment Tips your readers expect.

4. Plan for the Required Minimum Distributions (RMDs)

Starting at age 73, the government requires you to withdraw a portion of your traditional 401K and IRAs each year.

Key points to remember:

• RMDs are mandatory

• Roth IRAs do not have RMDs

• RMDs count as taxable income

• Proper planning helps avoid entering higher tax brackets

This is where a blended withdrawal plan (some from Roth, some from traditional) becomes powerful long-term Money Management Advice.

5. Build a Retirement Budget That Reflects the Real You

A joyful Retirement Budget isn’t about restriction — it’s about clarity.

Divide your spending into three categories:

Needs

Housing, utilities, food, insurance, taxes, healthcare

Wants

Dining out, hobbies, travel, entertainment

Dreams

Bucket-list trips, home upgrades, creative projects, meaningful retirement activities

This structure helps you protect your finances and the parts of life that make retirement fulfilling.

6. Control Your Taxes With Smart Sequencing

Taxes matter more in retirement than most people expect.

Here’s the simplest way to manage them:

Step 1: Withdraw from taxable accounts first

This keeps your tax rate more stable.

Step 2: Use Roth IRA withdrawals strategically

They’re tax-free and help you stay in lower brackets.

Step 3: Use traditional IRA/401K withdrawals to fill the gaps

This helps you avoid large RMDs later.

This method keeps your lifetime tax bill lower and stretches your savings further — a key part of smart Retirement Planning Insights.

7. Manage Inflation With Long-Term Growth

Inflation can slowly erode savings if your money isn’t growing.

To protect yourself:

• Keep part of your portfolio in stocks for long-term growth

• Review your spending once a year

• Adjust your Retirement Budget based on price changes

• Consider delaying Social Security because it offers inflation-adjusted income for life

Staying aware of inflation is essential for long, healthy financial planning.

8. Prepare for Rising Medical Costs

Healthcare becomes a bigger expense with age, so planning ahead keeps retirement peaceful.

Include these in your annual budget:

• Medicare Part B, Part D, and Medigap or Advantage plans

• Vision and dental care

• Prescription drugs

• Unexpected medical events

• Preventative and wellness care

• Long-term care planning

A yearly review of your medical spending keeps your plan accurate and aligned with your Money Saving Plan.

9. Keep Money Systems Simple and Joyful

Retirement money management doesn’t need to be complicated.

Here are small habits that make a big difference:

• Review spending monthly

• Rebalance your investments once a year

• Keep 6–12 months of emergency cash available

• Use a digital money tracker or simple notebook

• Stay organized with one central financial binder

• Discuss financial updates with your partner quarterly

These small habits create calm, clarity, and long-term security.

Your Most Confident, Joyful Retirement Starts Here 💛

Retirement isn’t just a financial milestone — it’s a new chapter of freedom, creativity, and everyday joy. With clear Retirement Planning Tips, smart decisions around when to retire, and practical steps to manage your money with confidence, you’re building a future that feels stable, meaningful, and beautifully yours.

If you want more inspiration for your next steps, explore these uplifting reads:

• Daily Schedule for Retirement Tips Every Retiree Needs

• Fun Retirement Activities for Women That Keep You Inspired

• What To Do When You’re Bored In Retirement (And Love It!)

Save this pin now so you can return to these joyful retirement planning insights anytime 💛